Increases in European blast furnace coke prices

There is much talk at present of the marked increases in world iron ore prices, in the last 12 months.

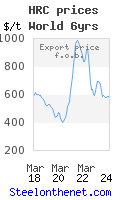

However, we notice that blast furnace coke prices have also increased very dramatically. European metallurgical coke has increased from ~$200/t at the start of the year, to near on $300/tonne in April 2021 (export prices, fob basis). That is equivalent to a price increase of around 50%.

For recent and historic European coke prices, visit us at https://www.steelonthenet.com/files/blast-furnace-coke.html.

Andrew M Kotas

Labels: blast furnace coke, coke, Europe, european, met coke, metallurgical coke, prices, steelmaking costs, steelmaking raw materials

posted by mci @ 2:31 PM permalink

0 comments

![]()

![]()