The Pittsburgh Post Gazette website carries the following story today, about the impact of Hurricane Katrina on US commodity prices, and on steel prices in particular. For original article, see

http://www.post-gazette.com/pg/05252/568475.stmWide range of commodities affected by post-hurricane disruptionFriday, September 09, 2005

The wrath of Hurricane Katrina's fury has been showing up at gas pumps for days, but in coming weeks, expect to pay considerably more to heat your home, build that new addition and stock up your refrigerator.

The Energy Information Administration, for example, predicted this week that home owners in the Midwest could expect to pay 71 percent more for natural gas to heat their homes this winter. In the Northeast, heating oil prices will be 31 percent higher.

Steel prices are rising, as are prices for wood, concrete, glass and other building materials, reflecting supply disruptions and shortages spawned both by damage and outages along Gulf ports and by an anticipated increase in demand for rebuilding.

Food crops were damaged in some areas, but the bigger issue is the cost of getting them from there to here now that fuel prices for all modes of transport are at record levels.

All this adds to the economic milieu that the Federal Reserve must consider as it weighs nudging up short-term interest rates to keep inflationary forces in check while acting to protect an economy reeling from Katrina's impact.

On one hand, the central bank must consider whether havoc wreaked by the storm could stall the economy. Already, the nonpartisan Congressional Budget Office has estimated that fallout from the hurricane will cost the economy some 400,000 jobs and shave about a percentage point off growth this year.

At the same time, economists expect all those sharply higher costs for energy, labor and materials -- all of which were climbing even before Katrina -- will begin working their way into consumer prices, making inflation a worsening concern. "I am looking for more of a pass-through" of all of those costs to the consumer, said Stuart Hoffman, chief economist for PNC Financial Services Group.

Still, while costs of many key commodities have been rising, their impact on key inflation measures is far less profound than that of increased labor costs, which rose at a 4.3 percent annual rate through the end of June, said Richard DeKaser, chief economist for Cleveland-based National City Corp. He initially thought the Fed would "wait out September" without raising rates to give the economy a breather from Katrina.

Since then, however, DeKaser said, remarks by some Fed district presidents, including Philadelphia's Anthony M. Santomero, have been "quite hawkish in their tones," suggesting inflation remains the central bank's main concern and that interest rate increases may continue unabated. PNC's Hoffman believes the Fed probably will raise rates once more, or possibly twice, this year.

Metals pricesFor metals producers, Katrina has presented a mixed bag. On the down side, higher energy prices will boost production costs, production at plants in the path of the storm will be crimped, and disruptions at the port of New Orleans, a key entry point for iron ore and other raw materials, could also affect metals producers outside the region.

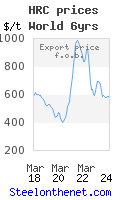

The higher energy prices are expected to curb demand for automobiles and appliances, two key markets for metals producers, acting as a sort of break on the ability of producers to pass through further price increases. U.S. Steel and other producers already have pushed through price increases of roughly 10 percent in recent weeks.

On the plus side, New Orleans is also a major port for steel imports and any delays in moving steel could give domestic steel prices unexpected strength.

A second big plus is that rebuilding will create demand for steel, aluminum, copper and other metals.

BB&T Capital Markets metals analyst Lloyd T. O'Carroll said that while it's too early to quantify rebuilding demand or say when orders will start rolling in, "it does appear to have large potential."

Energy will have the most immediate impact. Natural gas prices are now in the neighborhood of $12 per million BTUs compared with just under $10 before the storm, according to Global Insight senior economist John Mothersole. Two years ago, the commodity cost less than $6 per million BTUs.

It takes U.S. Steel about 4.4 million BTUs of gas to make a ton of raw steel, spokesman John Armstrong said.

O'Carroll said most metals producers hedge their natural gas costs to protect against volatile price swings. He said many steelmakers are protected for at least a year, so it comes down to whether those hedges will expire before natural gas prices subside.

John Anton, who keeps tabs on the steel industry for Global Insight, said he believes steelmakers who cater to the construction market will gain the most from Katrina. The storm gives their recent prices increases of about $60 per ton, or 10 percent, a better chance of sticking, he said. But he expects the higher prices will be short-lived.

Home building will boom in New Orleans, but it will not necessarily do any better anywhere else," he said.

Less fortunate are sheet steel suppliers serving the automotive and appliance markets, items consumers pinched by higher gasoline prices are less likely to purchase, Anton said.

Energy suppliesThe devastation wrought by Katrina on the nation's natural gas infrastructure should boost the fortunes of another form of energy, old King Coal.

With natural gas production severely crimped by the storm, electric power generators -- coal's largest customer -- will make more use of coal whenever possible, according to David Khani, managing director of the energy research group at the investment bank Friedman Billings Ramsey.

Oil, which also lost production capabilities to Katrina, could pick up a little bit of the power business but other alternatives, nuclear and hydroelectric, are already running pretty full out. "So coal is really going to be a big winner here,'' Khani, a certified financial analyst, said yesterday. "You will see coal pick up market share in the fall and winter and probably even in the spring."

More than 4 billion cubic feet per day of natural gas production, roughly 40 percent of the daily Gulf output, was shut in by the storm, according to the Minerals Management Service. Oil production was reduced by 861,000 barrels per day, or 57 percent of the usual 1.5 million barrels.

Coal prices were rising even before Katrina struck, thanks to increased domestic and international demand and the impact of higher costs for other forms energy.

Higher spot prices for coal eventually lead to higher prices under longer-term contracts as those contracts expire and are renewed, said Doug Biden, president of the Electric Power Generation Association, a trade group for electricity companies based in Harrisburg.

There was a lull in coal buying during August. Thomas Hoffman, vice president of external affairs for Upper St. Clair-based Consol Energy, said power generators were on the sidelines hoping for pricing to improve.

"But they're back in the market now because they know gas supplies are going to be tight and they're doing what they can to find coal," Hoffman said.

Higher coal prices are allowing Consol and other producers to expand. Consol, for example, has proposed spending about $500 million to enlarge its Enlow Fork mine near Washington, Pa.

The expansion, Consol's largest capital expenditure ever, would add 7 million tons of coal production capacity and support about 400 new mining jobs. The company's current annual production capacity is between 70 and 72 million tons.

RebuildingRebuilding the hurricane-pummeled region will take months or years, but the construction industry is already bracing for a surge in the cost of basic supplies such as plywood and cement.

Within two days of Katrina's hitting the Gulf Coast last week, it became harder to get quotes on orders, said Ron Mistik, purchasing director of Allegheny Millwork & Lumber on the South Side. "A lot of the plywood mills and OSB [oriented strand board] mills went off the market," he said.

Since then, most have come back on, said Jon Anderson, publisher of Oregon-based Random Lengths Publications, which tracks the wood products industry. While communications are still iffy, he said, his staff has documented only one plywood plant that was heavily damaged and is likely to be down for a number of weeks.

Yet the uncertainty may have driven contractors around the country with projects under way and deadlines to meet to replenish their inventories, which in turn put pressure on the supply and helped push prices up.

Just how significant Katrina's long-term impact on the market will be remains unknown.

The National Association of Home Builders noted the number of structures affected by Katrina is likely to dwarf those of past storms. Hurricane Andrew in 1992 destroyed more than 28,000 housing units, more than the combined total of four major hurricanes last year. Katrina and the subsequent floods may have damaged a large portion of the more than 200,000 homes in New Orleans alone beyond repair.

Based on the experience in past storms, the association is not predicting a massive, immediate surge in home building. Even the impact on supplies could be mixed, with disruption of mills possibly balanced by an influx of wood from toppled trees that might have to be harvested quickly.

The association did note than an estimated 12 percent of national cement imports came through New Orleans and Mobile. Cement supplies had already been strained this year.

At Washington County construction supply chain 84 Lumber Co., spokesman Jeff Nobers said some mills still aren't quoting prices for very far into the future because they are waiting to see what happens and those prices they are offering in the short term have risen.

"Is it a long-term increase? The suspicion is that it's not," said Nobers.

At Allegheny Millwork, Mistik is not so confident.

The company has plenty of supplies now to serve its customers but he believes inventories could be a bit slim in six to eight weeks. He is expecting the rebuilding process to have a bigger impact on prices and supplies than Hurricane Andrew did.

Truth is, the sheer size and reach of the destruction across the South means much of this is uncharted territory, he added. "My crystal ball's in the shop but I'll give you any information I have."

blogger@steelonthenet.com